AML Regulations for Estate and Letting Agents in the UK

AML Regulations for Estate and Letting Agents in the UK: At a Glance

- Estate agency businesses are within the scope of the Money Laundering Regulations 2017 and must register with HMRC before carrying on a regulated activity.

- Letting agency businesses come within the scope of the Money Laundering Regulations where the monthly rent is €10,000 or more, and the tenancy is for one month or longer.

- HMRC is the AML supervisor for estate agency businesses and for letting agency businesses that fall within the MLR threshold.

- Financial sanctions obligations are separate from MLR registration. OFSI guidance for letting agents states there is no monetary threshold for the relevant sanctions reporting obligation, and their reporting obligation starts from 14th May 2025.

- Core compliance duties include firm-wide risk assessment, customer due diligence, enhanced due diligence where required, ongoing monitoring, suspicious activity reporting, recordkeeping, internal controls, and staff training.

Who are Estate and Letting Agents under the UK’s AML Legal Framework?

For UK AML purposes, estate agency businesses and in-scope letting agency businesses are treated as separate categories of relevant persons under regulation 13 of the Money Laundering Regulations 2017.

Estate agency business is linked to estate agency work under the Estate Agents Act 1979, while letting agency business is defined separately in regulation 13 and only falls within MLR scope where the rent and term threshold is met.

What is an Estate Agency Business under the MLR 2017?

Under the AML regulations for estate agents, Regulation 13(1) of the MLR 2017 defines an estate agent as a firm or sole practitioner whose business carries out estate agency work as defined in section 1 of the Estate Agents Act 1979.

Estate Agents Act 1979, Section 1, defines estate agency work by reference to business activities carried out on instructions from another person to introduce, negotiate, or otherwise assist with the disposal or acquisition of an interest in land. Further, Section 2 of the Act explains what is meant by acquiring or disposing of interests in land, with the Act generally framed around UK land interests. However, MLR 2017, regulation 13, imports the section 1 concept into the AML regime, but expressly says that, for AML purposes, references to land transactions also include qualifying overseas property interests that are capable of separate ownership or holding.

For AML purposes, an estate agency business is a firm or sole practitioner carrying on estate agency work as defined by the Estate Agents Act 1979 and applied through regulation 13 of the MLR 2017. Broadly, this covers businesses acting on instructions to introduce parties to, or assist parties in acquiring or disposing of, interests in land, including certain overseas property interests recognised by the MLR framework.

Who is a Letting Agent Under the MLR 2017?

Under AML regulations for letting agents, Regulation 13(3) of the MLR 2017 defines a letting agent. A letting agency business is a firm or sole practitioner that carries out letting agency work in response to instructions from a prospective landlord or a prospective tenant. Under the Money Laundering Regulations 2017, a letting agency business must register with HMRC where the business handles lettings with individual rents of €10,000 or more per month and the tenancy is for one month or longer. This applies to both residential and commercial lettings.

HMRC’s risk guidance states that customer due diligence is required only in relation to lettings activity that falls within the regulation 13 threshold, including tenancies already above the threshold or those likely to exceed it during the tenancy.

Where a letting business operates below the regulation 13 threshold, it is generally outside MLR supervision as a letting agency business. That does not, by itself, remove potential sanctions, fraud, or other criminal law exposure. OFSI’s guidance for letting agents states that the relevant sanctions reporting obligation has no monetary threshold.

Examples of businesses that may fall outside AML registration as estate agency businesses include:

- Practising solicitors acting in the course of their professional duties

- Businesses that only publish property advertisements without participating in the transaction

- Platforms that simply allow buyers and sellers to contact each other directly

- Property developers selling their own properties within the same legal entity, as they are not acting as intermediaries between two parties.

Estate agency businesses must register with HMRC before carrying on regulated activity. Letting agency businesses must register with HMRC only where they fall within the regulation 13 threshold.

HMRC’s recently published penalty lists 2023 to 2024, 2024 to 2025, and 2025 to 2026 indicate that the vast majority of penalties imposed on estate agency businesses have related to failure to apply for registration at the required time under Regulation 56. As many as 332 of the 369 penalties were issued for unregistered trading. February 2026 HMRC penalty publication (covering April to September 2025) talks of 170 penalties against estate agency businesses totalling £835,842.

Key AML Laws and Regulations Applicable to Estate and Letting Agents in the UK

The principal legal framework for estate agency businesses and in-scope letting agency businesses is built around the Money Laundering Regulations 2017, POCA 2002, the Terrorism Act 2000, sanctions legislation made under SAMLA 2018, and the Estate Agents Act 1979 for the underlying definition of estate agency work. Depending on the transaction, firms should also consider transparency and ownership-related legislation such as the Economic Crime (Transparency and Enforcement) Act 2022 and the Economic Crime and Corporate Transparency Act 2023.

The AML Regulations for Estate and Letting Agents in the UK primarily comprise the following laws and regulations:

Sanctions and Anti-Money Laundering Act, 2018 (SAMLA)

- SAMLA 2018 sets the legal framework for how the UK applies sanctions after Brexit.

- For estate and letting agents, the day-to-day obligations usually come from the specific sanctions regulations and the related official guidance.

- Firms should have controls in place to identify designated persons.

- They must avoid entering into or supporting prohibited dealings.

- Where required, they must freeze relevant funds or economic resources.

- They must also make a report to OFSI when the legal reporting threshold is met.

The Money Laundering, Terrorist Financing and Transfer of Funds (Information on the Payer) Regulations 2017 (MLR)

- MLR 2017 is the core AML/CFT/CPF regulation applicable to Estate and Letting Agents in the UK.

- Estate agency businesses, and letting agency businesses that fall within regulation 13, are relevant persons under the MLR 2017 and must comply with the applicable AML, CFT and PF obligations under that regime.

- The key obligations for Estate and Letting Agents under MLR, 2017 include Risk Assessment, Customer Due Diligence, Policies and Procedures, Ongoing Monitoring, Record-Keeping, Staff Training and Suspicious Activity Disclosures requirements.

Proceeds of Crime Act, 2002 (POCA)

- POCA 2002 sets out the main money laundering offences in the UK.

- It also underpins the UK’s Suspicious Activity Report (SAR) regime.

- For estate and letting agents, this means concerns about criminal property may need to be reported through a SAR.

- Dealing with criminal property unlawfully can give rise to criminal liability.

- POCA 2002 also includes the offences of tipping off and prejudicing an investigation.

Terrorism Act, 2000

- The Terrorism Act 2000 is a key part of the UK’s counter-terrorist financing framework.

- It is relevant to estate and letting agents where there are suspicions involving terrorist property or terrorist financing.

- In such cases, firms may face reporting obligations.

- Prohibited conduct under the Act can also lead to criminal liability.

Terrorist Asset-Freezing etc. Act 2010 (TAFA 2010)

- The Terrorist Asset-Freezing etc. Act 2010 is a UK law that allows the government to freeze the funds and economic resources of persons suspected of involvement in terrorism.

- TAFA 2010’s purpose is to prevent such persons from using, moving, or benefiting from assets that could support terrorist activities.

- TAFA 2010 also makes related amendments to counter-terrorism legislation and provides the legal framework for enforcing these financial restrictions.

- It is important for estate agents and lettings agents need to comply with the requirements of TAFA 2010.

The Counter Terrorism (Sanctions) (EU Exit) Regulations 2019

- The Counter Terrorism (Sanctions) (EU Exit) Regulations 2019 require Estate and Letting Agents to identify accounts or assets belonging to designated persons, freeze such assets without delay and report any dealings with these persons to the relevant authorities.

- These regulations establish the UK’s post-Brexit terrorist asset-freezing regime under SAMLA.

Serious Organised Crime and Police Act, 2005

- The Serious Organised Crime and Police Act, 2005, strengthens AML/CFT obligations for Estate and Letting Agents by tightening Money Laundering laws and updating key legislation like POCA, 2002 and TACT, 2000.

- This means that Estate and Letting Agents in the UK must stay alert to suspicious transactions and report any concerns about ML or TF.

- The act also gives supervisory authorities stronger power to monitor financial activity and investigate crime.

Economic Crime (Transparency and Enforcement) Act 2022

- The Economic Crime (Transparency and Enforcement) Act, 2022, introduces measures to increase transparency in property ownership for Estate and Letting Agents.

- Under this act, Estate and Letting Agents must consider the Register of Overseas Entities when conducting due diligence on customers involved in UK property transactions and apply enhanced scrutiny where beneficial ownership structures are unclear.

Economic Crime and Corporate Transparency Act 2023

- The Economic Crime and Corporate Transparency Act, 2023, strengthens corporate transparency for Estate and Letting Agents and improves the reliability of information held by Companies House.

- Estate and Letting Agents under this act must consider new identity verification requirements for company directors and persons with significant control when conducting CDD on corporate clients.

Anti-Terrorism, Crime and Security Act, 2001

- The Anti-Terrorism, Crime and Security Act, 2001 frames the obligations for Estate and Letting Agents to comply with asset freezing orders and forbid the provision of funds or economic resources to prohibited parties.

Counter Terrorism Act 2008

- The Counter-Terrorism Act 2008 introduced powers for the Treasury to issue directions on jurisdictions of concern, including requirements to apply enhanced due diligence or restrict business with persons linked to specified countries. Some of these powers have been substantially superseded by the SAMLA 2018 framework and related sanctions regulations. However, other provisions, including terrorism-financing offences under Part 3, remain in force and form part of the wider CFT obligations applicable to estate and letting agents.

Counter-Terrorism and Security Act, 2015

- The Counter terrorism and Security Act, 2015, focuses on preventing terrorism and supports CFT obligations for Estate and Letting Agents by strengthening measures under the Terrorism Act, 2000.

Criminal Finances Act, 2017

- Criminal Finances Act, 2017 strengthens AML Compliance by allowing supervisory authorities to extend the freeze on suspicious transactions reported under the POCA, 2002.

- For Estate and Letting Agents in the UK, this means once a suspicious transaction is reported, they must not proceed with it for an extended period, making strict compliance with internal controls essential to avoid legal risks.

- The act also gives enforcement bodies like NCA and FCA stronger powers to investigate and block suspicious funds for longer while building a case.

Estate Agents Act, 1979

- The Estate Agents Act 1979 provides the legal meaning of estate agency work used for estate agency businesses. Letting agency business is separately defined in regulation 13 of the MLR 2017.

- The Estate Agents Act provides a legal basis to MLRs to define the covered activities of estate agents for AML/CFT/CPF compliance.

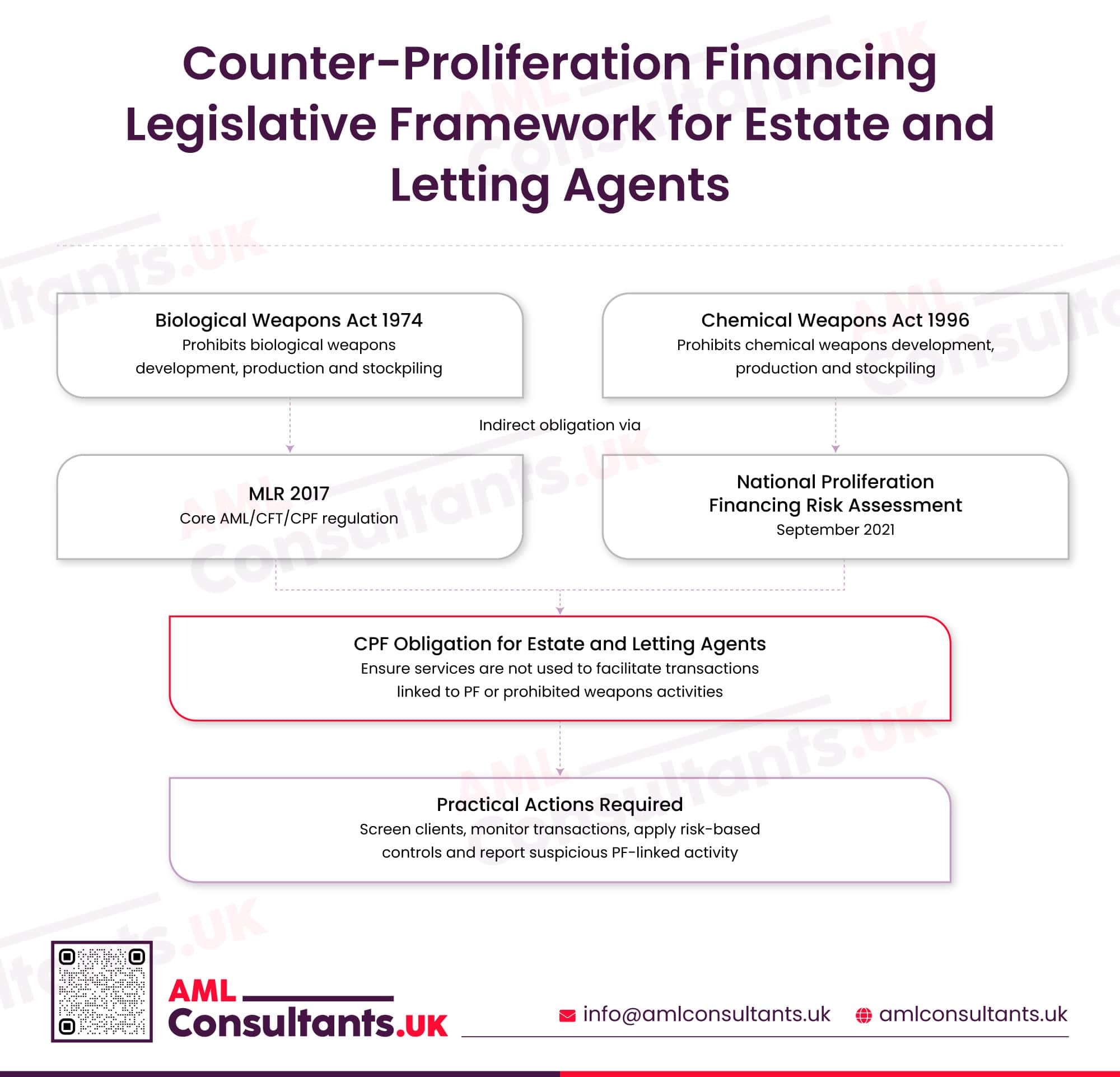

Counter-Proliferation Financing Legislative Framework for Estate and Letting Agents

Biological Weapons Act 1974

- Although primarily for national security, this law puts an indirect obligation via MLR 2017 and National Proliferation Financing Risk Assessment on Estate and Letting Agents to ensure that the services of estate and letting agents are not used to facilitate transactions linked to prohibited biological weapons activities or Proliferation Financing.

Chemical Weapons Act 1996

- Under the Chemical Weapons Act, 1996, Estate and Letting Agents must remain vigilant for transactions that may indicate Proliferation Financing or the funding of activities connected to chemical weapons development or procurement. This one is also an indirect obligation via MLR 2017 and National Proliferation Financing Risk Assessment on Estate and Letting Agents.

Simplify AML/CFT/CPF Compliance for Your Real Estate and Letting Agency

Get Clear and Practical Guidance to Meet Regulatory Expectations

AML/CFT/CPF Guidance Applicable to Estate and Letting Agents

The most useful guidance for this sector includes HMRC’s registration and supervision guidance for estate agency businesses and letting agency businesses, HMRC’s estate and letting agency business guidance for money laundering supervision, the UK National Risk Assessment, and OFSI’s financial sanctions guidance for letting agents.

Under AML Regulations for Estate and Letting Agents in the UK, the following are the general and sector-specific guidance issued by various authorities:

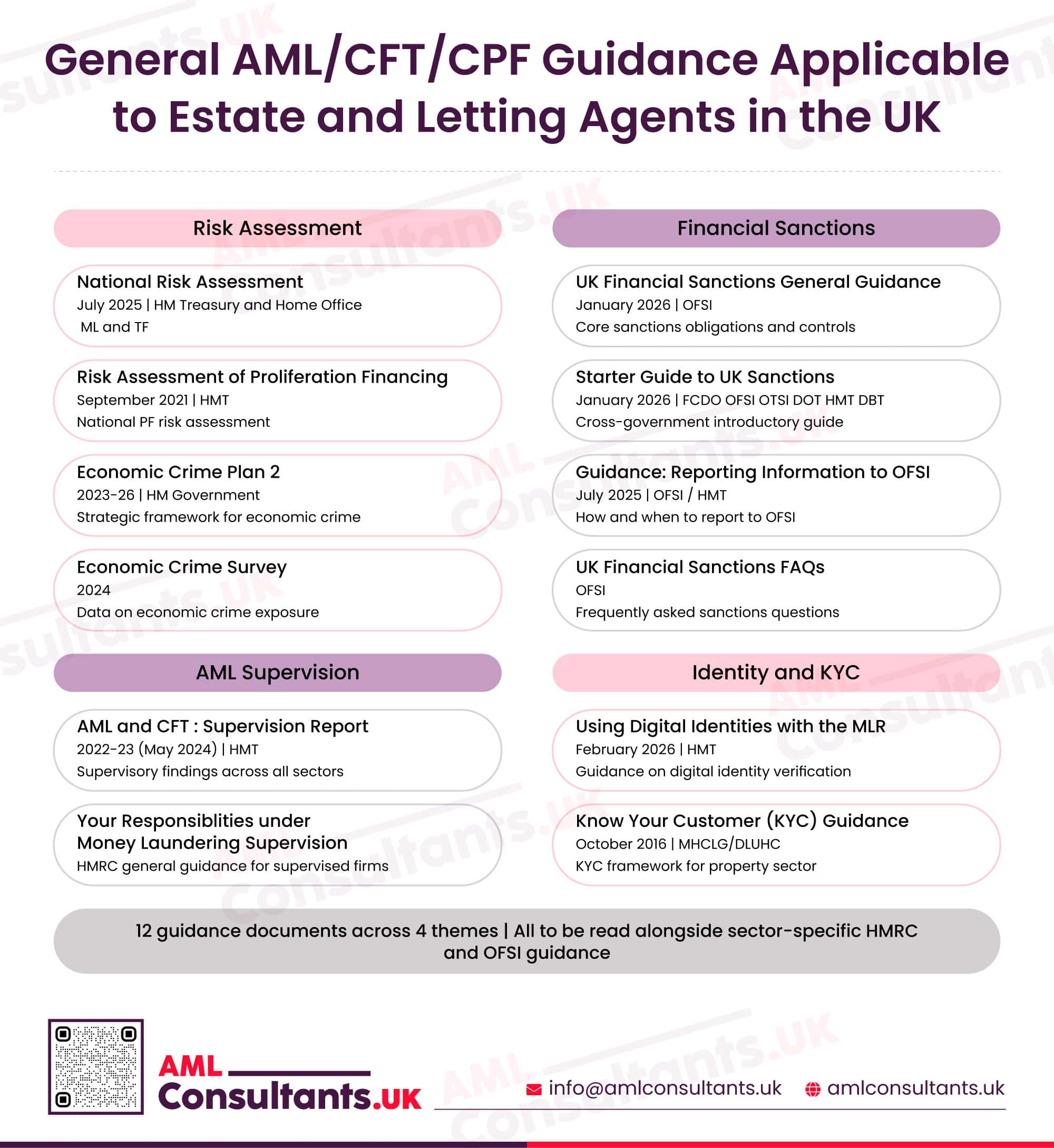

General Guidance:

- National Risk Assessment of Money Laundering and Terrorist Financing July 2025

- UK Financial Sanctions General Guidance January 2026

- HMT Risk assessment of proliferation financing September 2021

- HMT AML and CFT: Supervision Report: 2022-23 (May 2024)

- HM Government Economic Crime Plan 2 2023-26

- Economic Crime Survey 2024

- FDCO OFSI OTSI DoT HMT DBT Starter Guide to UK Sanctions January 2026

- OFSI HMT Guidance Reporting Information to OFSI July 2025

- HMT Guidance Using digital identities with the Money Laundering Regulations February 2026

- MHCLG HE MHCLG DLUHC Guide on ‘Know your customer’ guidance – October 2016

- Guidance: Your responsibilities under money laundering supervision

- Guidance: UK Financial Sanctions FAQs

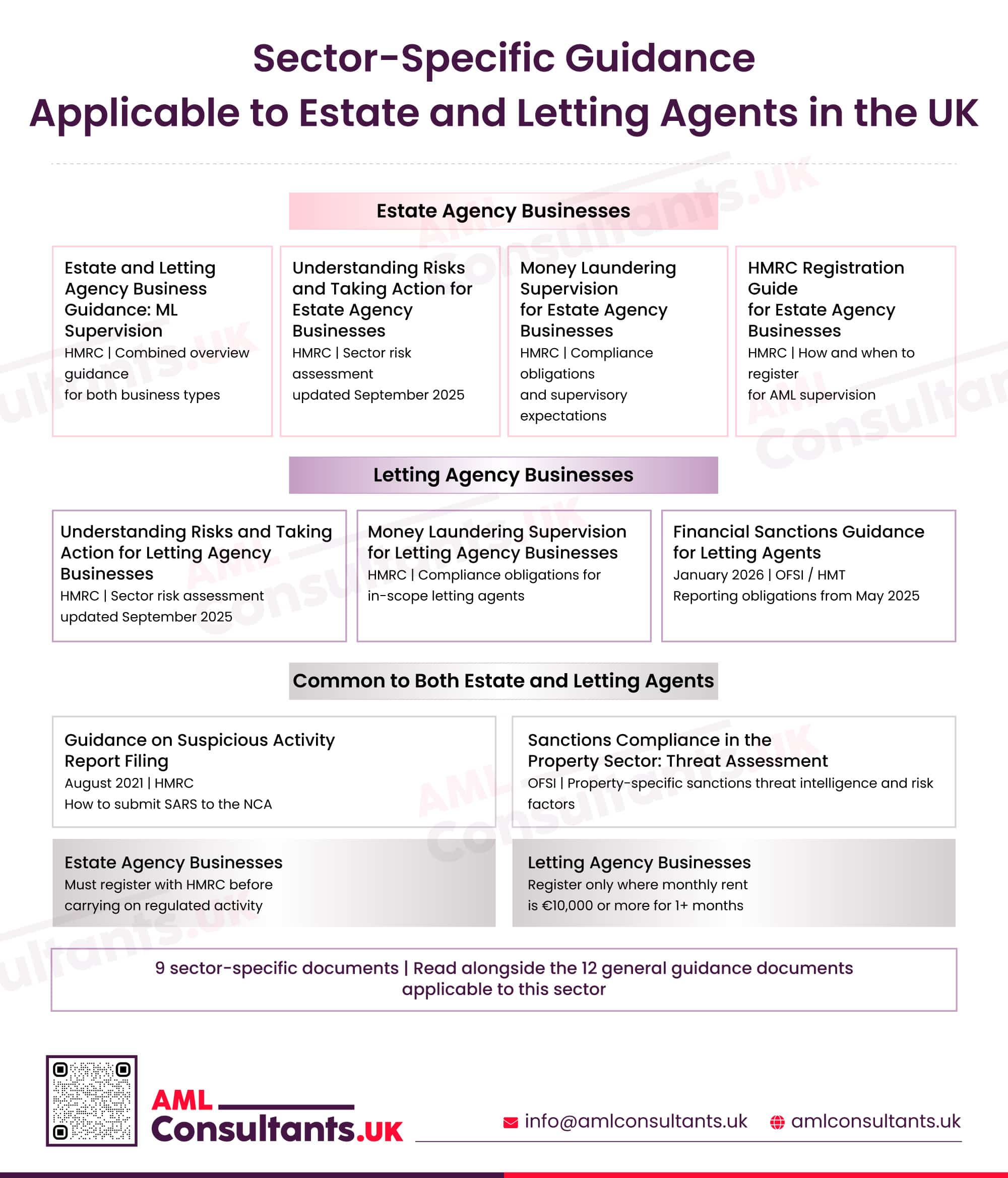

Specific Guidance:

- Estate and letting agency business guidance, money laundering supervision

- Guidance: Understanding risks and taking action for estate agency businesses

- Guidance: Understanding risks and taking action for letting agency businesses

- Guidance: Money laundering supervision for estate agency businesses

- Guidance: Money laundering supervision for letting agency businesses

- OFSI HMT Financial sanctions guidance for letting agents January 2026

- HMRC registration guide for estate agency businesses

- Sanctions compliance in the property sector: threat assessment

Supervisory Authority for Estate and Letting Agents within AML Regulatory Framework for Estate and Letting Agents in the UK

Often, the question arises, who supervises estate agents and letting agents from an AML perspective? It is His Majesty’s Revenue and Customs (HMRC) that oversees compliance with the AML Regulations for Estate and Letting Agents in the UK.

As part of their AML obligation, Estate and Letting Agents must register with HMRC.

The HMRC’s responsibilities towards Estate and Letting Agents include:

- Monitoring the AML compliance of Estate and Letting Agents

- Issuing guidelines and other directives for Estate and Letting Agents pertaining to AML obligations

- Conducting regular inspections of Estate and Letting Agents

- Imposing penalties or other enforcement actions for regulatory breaches on Estate and Letting Agents

The HMRC AML supervision for estate agents and letting agents helps ensure legal compliance and effective counter-measures against money laundering and terrorist financing.

The Office of Financial Sanctions Implementation (OFSI) oversees the financial sanctions compliance of Estate and Letting Agents.

From 14 May 2025, letting agents became subject to a relevant-firm reporting obligation for UK financial sanctions purposes. OFSI guidance states that there is no monetary threshold for this reporting obligation. Where a letting agent knows or has reasonable cause to suspect that a person is a designated person, or that a breach of financial sanctions has occurred, it must report to OFSI as soon as practicable in line with the applicable regulations.

OFSI’s published guidance for letting agents clarifies that the reporting obligation arises at two specific points in the transaction: when a landlord instructs the letting agent, and when a landlord accepts a prospective tenant’s offer. There is no obligation under the relevant sanctions reporting framework to report on a tenant before their offer has been accepted by the landlord. Estate and letting agents should ensure their compliance procedures and client intake workflows are designed to reflect these trigger points, so that the obligation is met at the correct stage of the transaction rather than applied inconsistently across the letting process.

Get Your AML Regulatory Reporting Done the Right Way!

From SAR Submission, OFSI Reporting to HMRC Responses, Ensure Your Filings Are Complete, Accurate and Compliant.

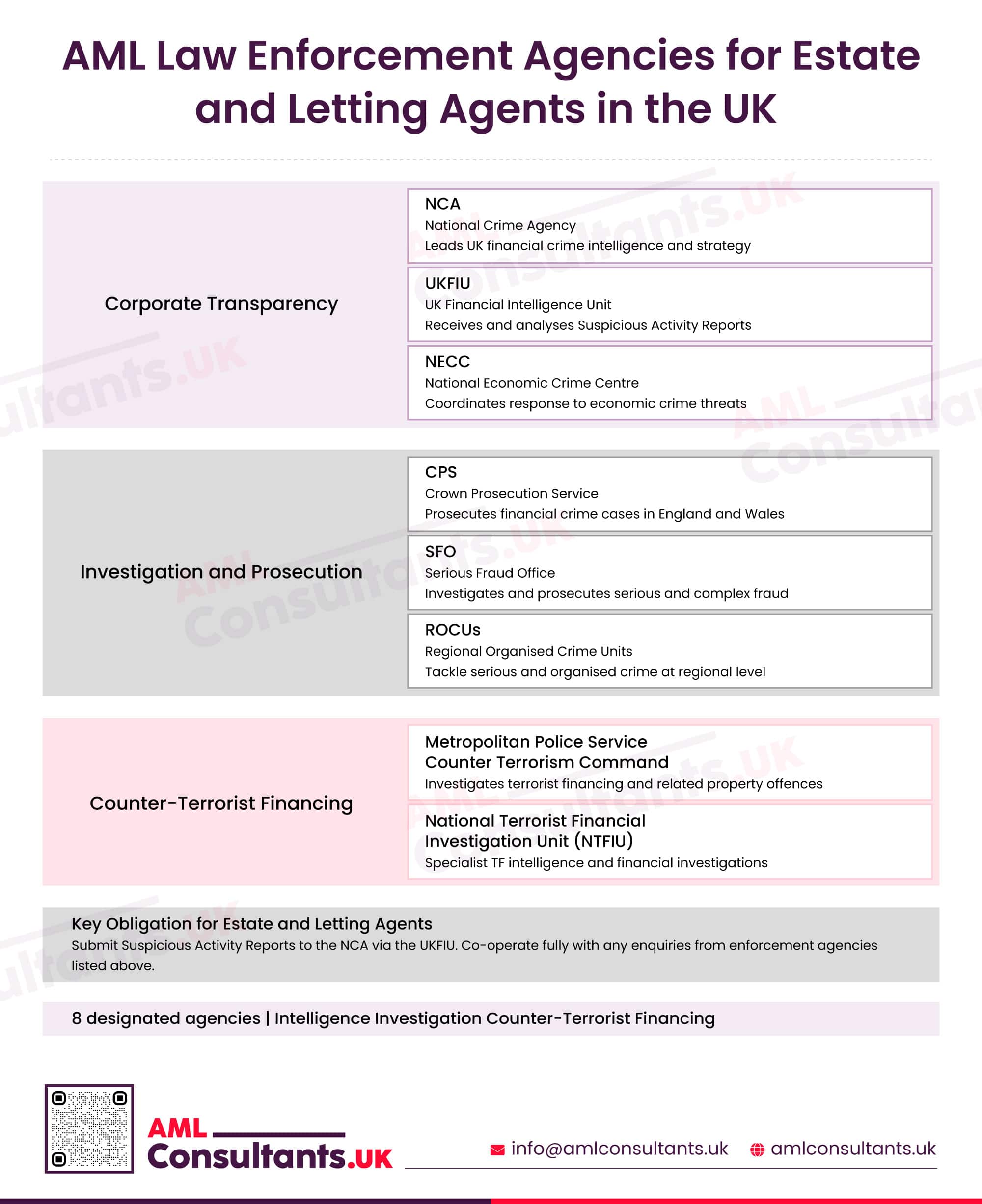

AML Law Enforcement Agencies for Estate and Letting Agents in the UK

In line with Anti-Money Laundering Laws for Estate and Letting Agents in the UK, Financial crime intelligence and investigations in the UK are handled by several designated Law Enforcement Agencies, which are as follows:

- National Crime Agency (NCA)

- UK Financial Intelligence Unit (UKFIU)

- National Economic Crime Centre (NECC)

- Crown Prosecution Service (CPS)

- Serious Fraud Office (SFO)

- Regional Organised Crime Units (ROCUs)

- Metropolitan Police Service (Counter Terrorism Command)

- National Terrorist Financial Investigation Unit (NTFIU)

Administrative Bodies in UK for Estate and Lettings Agents

For HMRC-supervised estate and letting agents in the UK, here is the list of administrative bodies:

Implications of UK’s National Risk Assessment on Estate and Letting Agents

The 2025 UK National Risk Assessment indicates that the wider property sector remains highly exposed to money laundering risk, with estate agency businesses identified as among the more exposed sub-sectors.

The National Risk Assessment of Money Laundering and Terrorist Financing 2025, issued by HM Treasury, identifies Estate Agency businesses as Medium-Risk for Money Laundering and Low-Risk for Terrorism Financing activities. Whereas Letting Agency businesses are identified as Low-Risk for the ML/TF activities. However, the NRA 2025 has assessed the property sector overall as posing a higher risk of money laundering, with letting agents identified as one of the property sectors with the highest risk of exposure.

While estate agency businesses themselves are rated medium risk, the NRA 2025 rates the wider UK property sector as high risk for money laundering, with estate agents identified as among the most exposed sub-sectors.

For HMRC-supervised Estate Agents, the risk of ML has risen slightly since the last NRA. While most agents do not handle client money directly, their role in identifying the true buyer and seller is vital. A major implication for this sector is the increasing complexity of transactions involving private investment vehicles and offshore structures that can hide a buyer’s identity.

The NRA highlights super prime properties as red flags, as these are often bought by Politically Exposed Persons (PEPs) or overseas buyers using funds from high-risk jurisdictions. Online banking and remote property viewing have also created new vulnerabilities, as criminals use AI to create fake identities to bypass identity checks during the onboarding process.

For HMRC-supervised letting agents, the NRA 2025 assesses LAB services themselves as low risk, consistent with the NRA 2020. However, the risks to which letting agents are exposed remain significant and unchanged from the previous assessment. The NRA 2025 identifies letting agents as one of the property sectors with the highest risk of exposure to the money laundering risks generated by the wider property market. This exposure is heightened by the fact that most letting agents handle client money directly, including deposits, fees, and rent, and funds in the lettings market move quickly, sometimes on the same day as a viewing. The anonymity of landlords and tenants, the potential involvement of offshore accounts, and the use of layered corporate structures to obscure beneficial ownership all contribute to this elevated exposure profile.

Estate and Letting Agents are required under the AML Regulations for Estate and Letting Agents in the UK to take NRA findings into account while conducting their own ML/TF/PF Risk Assessment. Both the NRA and their own risk assessment findings should be used to put in place internal controls, policies and procedures to mitigate identified ML/TF/PF risks.

Further, the estate agents and letting agents should also consider the National Risk Assessment of Proliferation Financing, September 2021 and implement their CPF controls.

Strengthen Your Internal AML Governance Structure

Get Expert Support to Build Your AML Department, Implement Controls and Manage Compliance Confidently In-House.

FATF Recommendations Concerning Estate and Letting Agents in the UK

The UK is a dedicated member of the Financial Action Task Force (FATF). The UK’s AML regime is shaped by international standards set by the FATF, including the standards applicable to real estate agents as DNFBPs in practice. Estate and letting agents comply with FATF-aligned expectations through the UK’s domestic laws, regulations, and guidance rather than by applying FATF Recommendations directly as standalone legal obligations.

The FATF recommendation 22 covers DNFBPs, including real estate agents. FATF Recommendation 12 (PEPs) and Recommendation 15 (new technologies / virtual assets) are increasingly relevant to the property sector, given the NRA 2025 commentary on AI-enabled identity fraud and the use of complex structures by PEPs. FATF Recommendations set the international standards relevant to real estate agents as DNFBPs. In the UK, those standards are implemented through domestic laws, regulations and guidance rather than applying directly as standalone legal obligations. Accordingly, regulated businesses must ensure

- Adherence to the UK’s national AML/CFT/CPF laws and regulations

- Assessment of an ML/TF/PF risk exposure of the business and adoption of a Risk-Based Approach

- Establishment of AML/CFT/CPF policies, controls and procedures

- Undertaking Customer Due Diligence

- Application of Targeted Financial Sanctions obligations arising under applicable UN and UK sanctions frameworks.

- Administering Enhanced Due Diligence on high-risk customers such as PEPs, clients from high-risk jurisdictions, etc.

- Reporting Suspicious Activities or Transactions to the authorities

- Maintaining Records of measures taken

The AML Regulations for Estate and Letting Agents in the UK mandate them to comply with these measures.

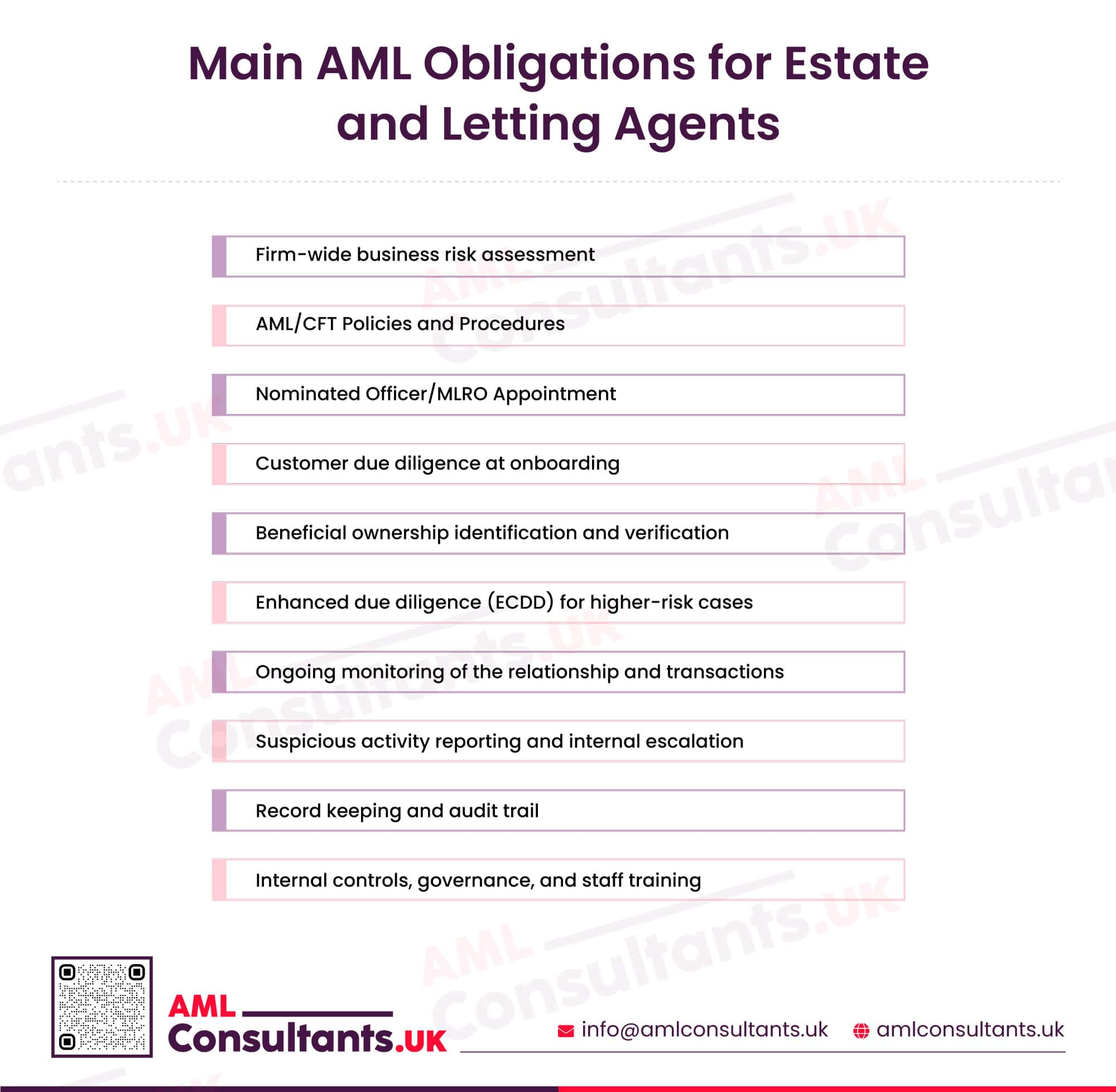

Main AML Obligations for Estate and Letting Agents

Estate agency businesses and letting agency businesses that fall within the Money Laundering Regulations 2017 threshold need more than a legal awareness of AML rules. They need working controls that can be demonstrated in practice. They need to appoint a nominated officer/MLRO to carry out AML compliance functions.

HMRC’s guidance for estate and letting agency businesses specifically points to customer due diligence, record keeping, and suspicious activity reporting as core parts of compliance, while the wider MLR framework also requires firms to assess risk, apply enhanced measures where needed, maintain policies, procedures, and internal controls, and train relevant staff.

In practical terms, this means the business should carry out a firm-wide risk assessment, identify and verify customers and beneficial owners, understand the purpose of the relationship or transaction, and apply enhanced due diligence where the risk profile is higher.

Firms should also keep customer information up to date through ongoing monitoring, know when and how to escalate concerns into a suspicious activity report, maintain proper records, and ensure staff understand the warning signs relevant to the property sector.

HMRC’s supervision material makes clear that the extent of CDD should be appropriate to the risks identified by the firm and the sector.

AML scope versus sanctions scope for letting agents

This distinction is important because many readers wrongly assume that if a letting business is below the €10,000 monthly rent threshold, it sits outside all financial crime obligations.

That is not the right way to look at it.

Under HMRC’s guidance, a letting agency business must register for AML supervision where the individual rent is €10,000 or more, and the tenancy is for one month or longer. Businesses below that threshold are generally outside the MLR registration scope for letting agency business.

However, sanctions obligations should be considered separately from AML registration under the MLRs.

A business may be out of scope for MLR registration as a letting agency business, yet still needs to think carefully about financial sanctions obligations and sanctions-related controls. This separation of AML scope and sanctions scope is one of the most important practical clarifications in the property sector, where firms often confuse the rent threshold with overall financial crime exposure.

Key point:

The €10,000 monthly rent threshold is relevant to MLR registration for letting agency business. It should not be treated as a universal threshold for all financial crime obligations.

AML Laws for Estate and Letting Agents: Roadmap to Navigate this Guide

Follow the map to discover the sector-specific AML legal and compliance framework for Estate and Letting Agents.

Central Framework | Relevant Person | Supervisory Authority | Sector-Specific Compliance Requirements |

| Estate and Letting Agents | HMRC | AML Compliance Requirements for Estate and Letting Agents in the UK |

How AML Consultants UK Supports Smooth Implementation of AML Regulations for Estate and Letting Agents in the UK

Estate and Letting Agents are required to foster an approach that translates into effective internal control and practical execution of the AML/CFT/CPF compliance measures. Even small gaps in compliance can result in hefty regulatory penalties and increased exposure to ML/TF/PF risks.

AML Consultants UK is a leading global AML/CFT/CPF consultancy firm offering a wide range of expert governance, risk and compliance services to support the smooth implementation of AML Regulations for Estate and Letting Agents in the UK.

From helping Estate and Letting Agents to conduct extensive Firm-Wide Risk Assessments, to building strong internal policies, controls and procedures to mitigate identified ML/TF/PF risks, there is no one in business like AML Consultants UK.

The skilled experts in AML Consultants UK understand AML Regulations for Estate and Letting Agents in the UK intricately and provide insightful and practical advice to the businesses, which helps them navigate the complex legal requirements effortlessly.

Equip Your Team to Handle AML Responsibilities Effectively

Provide Practical, Role-Based Training covering CDD, SAR Reporting, Sanctions and Red Flags Identification

FAQs: AML Regulations for Estate Agents and Letting Agents in the UK

Do the UK’s Money Laundering Regulations apply to estate agents?

Yes. Estate agency businesses are within the scope of the Money Laundering Regulations 2017 and must register with HMRC before carrying on regulated activity.

What are the AML Regulations for Estate and Letting Agents in the UK?

For this sector, the AML framework is mainly made up of the Money Laundering Regulations 2017, POCA 2002, the Terrorism Act 2000, UK sanctions legislation and guidance, HMRC supervision, and sector-specific government guidance.

Which laws regulate AML compliance for Estate and Letting Agents in the UK?

The main laws are Sanction and Anti-Money Laundering Act, 2018 (SAMLA 2018), The Money Laundering, Terrorist Financing and Transfer of Funds (Information on the Payer) Regulation 2017 (MLR 2017), Proceeds of Crime Act, 2002 (POCA 2002), Terrorism Act, 2000, the relevant UK sanctions regulations, and the Estate Agents Act, 1979 for estate agency work. Depending on the transaction, the Economic Crime (Transparency and Enforcement) Act 2022 and the Economic Crime and Corporate Transparency Act 2023 may also be relevant.

Do letting agents fall under the UK AML regulatory framework?

Yes, but not all in the same way. Letting agency businesses come within the MLR registration regime where rents are €10,000 or more per month, and the tenancy lasts one month or longer. Separately, OFSI guidance for letting agents confirms that the relevant sanctions reporting obligation has no monetary threshold.

Who supervises the compliance with AML Regulations for Estate and Letting Agents in the UK?

HMRC supervises estate agency businesses and in-scope letting agency businesses under the Money Laundering Regulations. OFSI is the relevant authority for UK financial sanctions reporting obligations.

Do estate and letting agents need to register with HMRC for AML/CFT/CPF supervision?

Estate agency businesses must register with HMRC before carrying on regulated activity. Letting agency businesses must also register where they meet the MLR threshold.