AML Legal Framework in UK

AML Legal Framework in the UK: What’s in Store

- The UK has a well-established AML Legal Framework built to prevent ML/TF/PF activities.

- Core laws and regulations include SAMLA 2018, MLR 2017, POCA 2002, TACT 2000 and several other acts that collectively shape the AML Legal Framework in the UK.

- This extensive framework is supervised by multiple supervisory authorities such as FCA, HMRC, the Gambling Commission and various professional bodies.

- Businesses classified as “Relevant Persons” in the UK must implement compliance measures under the AML Legal Framework in the UK.

Overview of UK’s AML Laws and Regulations

The United Kingdom has established a comprehensive Anti-Money Laundering (AML), Counter-Terrorist Financing (CFT) and Counter Proliferation Financing (CPF) framework to prevent, detect and disrupt the illegal financing of money.

The extensive AML Legal Framework in the UK is built upon a combination of primary laws, executive regulations, supervisory oversight, enforcement mechanisms and government strategies. The driving factor behind this vast legislative framework is international standards established by the Financial Action Task Force (FATF).

The UK has deployed a Risk-Based Approach in architecting its AML Legal Framework, which consists mainly of compliance requirements for Relevant Persons.

The key compliance obligations for Relevant Persons under AML Legal Framework in the UK are Risk Assessment, Customer Due Diligence (CDD), Suspicious Activity Disclosures, Record-Keeping, Sanctions Compliance and establishment of a dedicated AML/CFT/ CPF program.

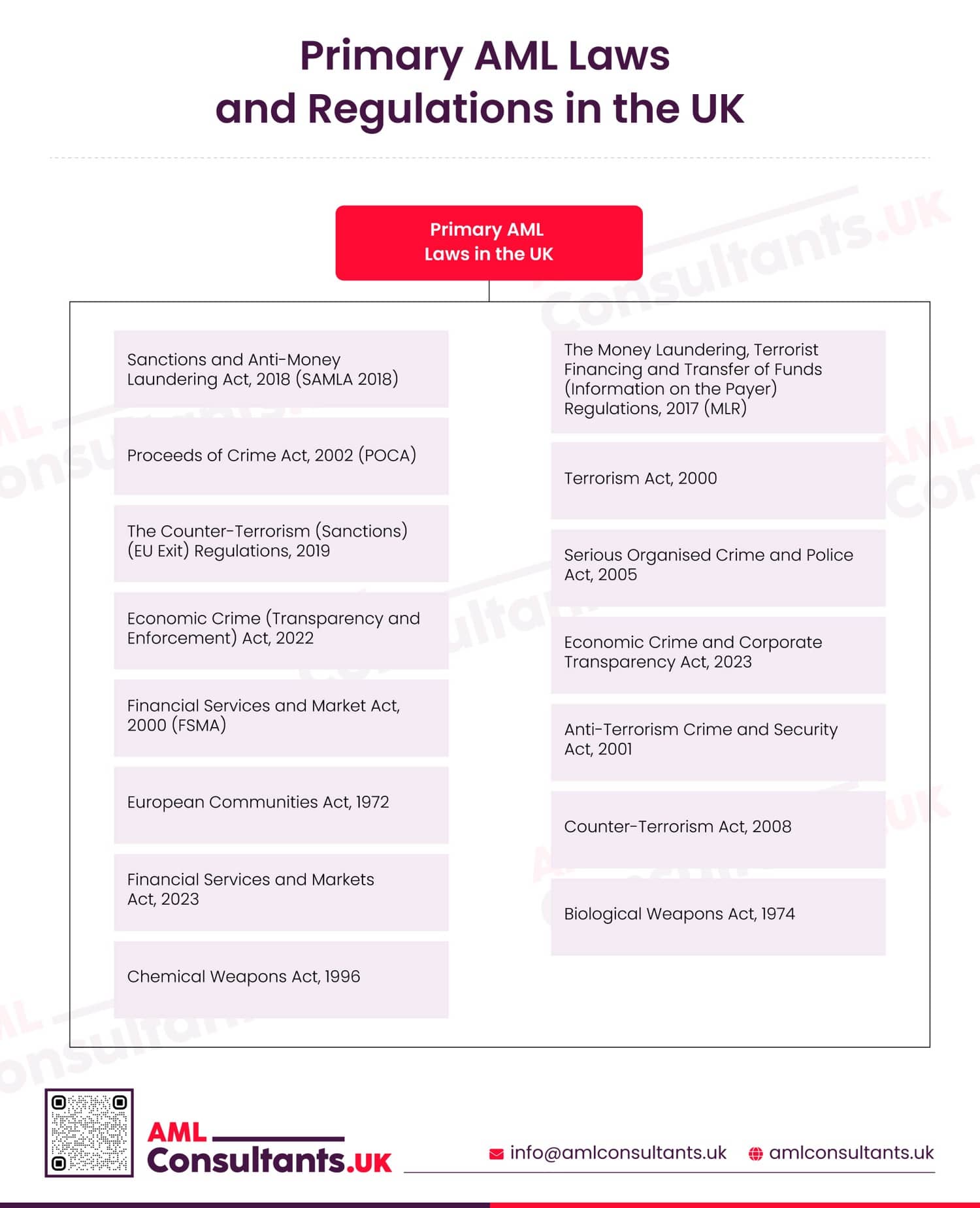

Primary AML Laws and Regulations in the UK

Major laws and regulations forming the AML Legal Framework in the UK are as follows:

Sanctions and Anti-Money Laundering Act, 2018 (SAMLA 2018)

SAMLA 2018 establishes the UK’s independent framework for imposing sanctions and making AML regulations after Brexit. It empowers the government to mandate CDD obligations, authorise supervisors such as the FCA and HMRC to oversee compliance, and enforce civil and criminal penalties.

The Money Laundering, Terrorist Financing and Transfer of Funds (Information on the Payer) Regulations, 2017 (MLR 2017)

The MLR, 2017, is the main operational AML regulation in the UK. It defines “Relevant Persons” and imposes obligations such as Risk Assessment, CDD, internal policies, procedures, and controls, and record-keeping and reporting.

It has been amended several times to address Brexit adjustments, crypto assets, Proliferation Financing, PEP treatment and alignment with FATF high-risk country lists.

Proceeds of Crime Act, 2002 (POCA)

POCA forms the core criminal law framework for Money Laundering in the UK. It establishes key offences relating to concealing, arranging or possessing criminal property and provides powers for confiscation and asset recovery with severe penalties.

Terrorism Act, 2000

This act establishes the primary legal basis for Terrorist Financing offenses in the UK. It criminalises dealing with terrorist property and requires individuals to disclose knowledge or suspicion of terrorist financing.

The Counter-Terrorism (Sanctions) (EU Exit) Regulations 2019

These regulations establish the UK’s post-Brexit terrorist asset-freezing regime under SAMLA. It allows the Treasury to designate persons involved in terrorism and require Relevant Persons to report suspected breaches or dealings with designated individuals.

Serious Organised Crime and Police Act 2005

This Act strengthened the UK’s response to organised crime and refined certain money laundering provisions linked to POCA. It introduced additional investigative and enforcement powers to support financial crime investigations.

Economic Crime (Transparency and Enforcement) Act 2022

This Act introduced the Register of Overseas Entities to improve transparency of foreign ownership of UK property. It also strengthened the Unexplained Wealth Order regime and enhanced enforcement powers against illicit wealth.

Economic Crime and Corporate Transparency Act 2023

This legislation strengthens corporate transparency by introducing identity verification for company directors and persons with significant control. It also enhances Companies House powers, updates the overseas entities register, and introduces provisions relating to crypto assets.

Financial Services and Market Act, 2000 (FSMA)

While primarily for financial regulations, it provided the initial legal powers for the Treasury to make the Money Laundering Regulations and granted power to the FCA (Financial Conduct Authority) to enforce them.

Anti-Terrorism, Crime and Security Act, 2001

This Act provides powers to freeze assets of overseas persons or governments threatening the UK economy. It also includes provisions addressing proliferation financing related to weapons of mass destruction.

European Communities Act, 1972

This Act historically enabled the UK to implement EU legislation domestically. It provided the original legal basis for the Treasury to introduce Money Laundering Regulations aligned with EU AML directives.

Counter-Terrorism Act 2008

This Act allows the Treasury to require financial institutions to apply enhanced due diligence or restrict business with persons linked to high-risk jurisdictions. It also addresses risks relating to proliferation financing and weapons development.

Financial Services and Markets Act 2023

This Act reforms financial services regulations post-Brexit and introduces amendments affecting AML/CFT obligations. It requires updates to the MLR 2017, including provisions that treat domestic politically exposed persons (PEPs) as lower risk unless specific risk factors exist.

Biological Weapons Act 1974

- This Act prohibits the development, production, acquisition, or possession of biological weapons and related agents except for peaceful purposes.

- Although primarily for national security, this law puts an obligation on Relevant Persons to ensure that their services are not used to facilitate transactions linked to prohibited biological weapons activities or Proliferation Financing.

Chemical Weapons Act 1996

This Act implements international obligations relating to chemical weapons and criminalises their development, production, possession, or use. It establishes strict prohibitions and penalties, including life imprisonment for serious offences.

Strengthen your AML compliance framework

Design practical policies, controls, and procedures that support effective compliance and day-to-day implementation

TFS Measures Implementing Regime under AML Legal Framework in the UK

Under the AML Legal Framework in the UK, the Targeted Financial Sanctions (TFS) framework is mainly integrated in SAMLA 2018, which gives the government the power to create and enforce its own sanctions regimes.

Along with SAMLA 2018, Counter-Terrorism Act, 2008 and Terrorist Act, 2000 are other substantial legislation for sanctions compliance. These laws lay down the requirements for asset freezing and prohibit the provision of any funds to the designated individuals or entities. These obligations apply to all individuals and businesses in the UK.

The Office of Financial Sanctions Implementation (OFSI) is responsible for implementing and managing financial sanctions in the UK. It maintains the UK Consolidated List of sanctioned people and establishes a reporting obligation for Relevant Persons to inform OFSI as soon as there is a target match with the designated person.

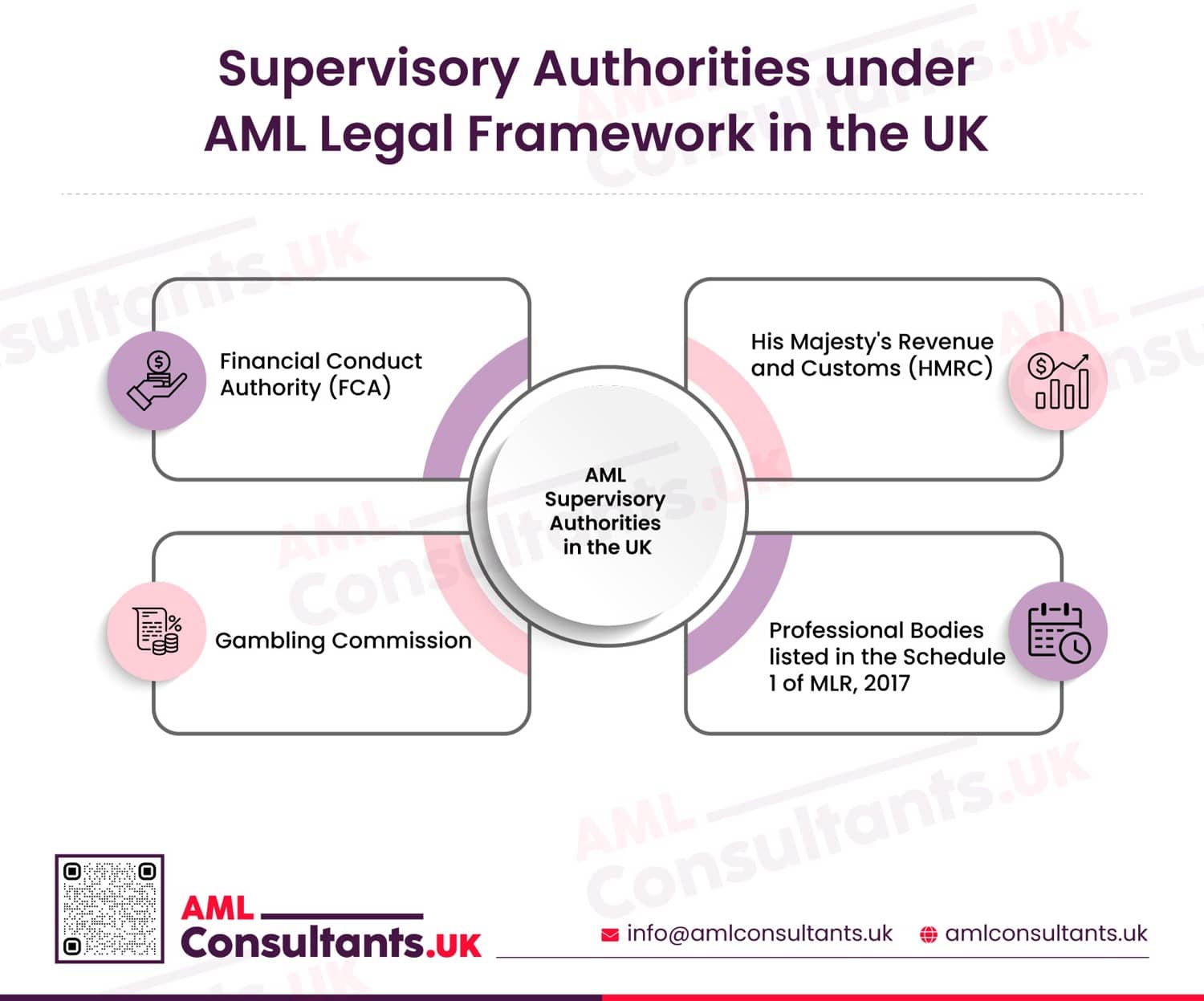

Supervisory Authorities under AML Legal Framework in the UK

The AML Legal Framework in the UK recognizes 3 main government bodies which oversee the compliance of AML legal framework as explicitly defined in Regulation 7 of MLR, 2017.

These are:

Financial Conduct Authority (FCA):

FCA in the UK supervises the following sectors:

- Credit and Financial Institutions

- Crypto assets exchange provider

- Custodian wallet providers

- Auction Platforms

His Majesty’s Revenue and Customs (HMRC):

HMRC in the UK supervises the following sectors:

- High-value dealers

- Money Service Businesses (provided they are not supervised by the FCA)

- Trust or Company Service Providers (TCSPs) (provided they are not supervised by FCA or other supervisory body)

- Auditors, external accountants and tax advisors (provided they are not supervised by any of the professional bodies)

- Bill payment service providers (which are not supervised by the FCA)

- Telecommunication, IT and digital service providers (provided they are not supervised by FCA)

- Real Estate and Letting Agencies (Which are not supervised by professional bodies)

- Art market participants

Gambling Commission:

The Gambling Commission in the UK supervises the following sector:

- Casinos

Professional Bodies Listed in Schedule 1 of MLR, 2017

There are 22 other Professional bodies listed in Schedule 1 of MLR, 2017 that supervise specific professional services.

Office for Professional Bodies Anti-Money Laundering Supervision (OPBAS) is an oversight body that ensures the 22 professional bodies maintain high and consistent standards.

Supervisory Professional Bodies for Accountancy, Auditing and Bookkeeping Sector:

- Association of Accounting Technicians

- Association of Chartered Certified Accountants

- Association of International Accountants

- Chartered Institute of Management Accountants

- Institute of Certified Bookkeepers

- Institute of Chartered Accountants in England and Wales

- Institute of Chartered Accountants in Ireland

- Institute of Chartered Accountants of Scotland

- Institute of Financial Accountants

- International Association of Bookkeepers

Supervisory Professional Bodies for the Legal Sector:

- Chartered Institute of Legal Executives

- Council for Licensed Conveyancers

- Faculty of Advocates

- Faculty Office of the Archbishop of Canterbury

- General Council of Bar

- General Council of the Bar of Northern Ireland

- Law Society (England and Wales)

- Law Society of Northern Ireland

- Law Society of Scotland

Supervisory Professional Bodies for the Taxation Sector:

- Association of Taxation Technicians

- Chartered Institute of Taxation

Supervisory Professional Bodies for Insolvency Practitioners:

- Insolvency Practitioners Association

Law Enforcement Agencies within AML Legal Framework in the UK

AML Legal Framework in the UK is supported by several law enforcement agencies. These agencies are responsible for investigating ML/TF/PF and related financial crimes.

The following are the law enforcement agencies under UK’s AML Regulations:

- National Crime Agency (NCA)

- UK Financial Intelligence Unit (UKFIU)

- Office of Financial Sanctions Implementation (OFSI)

- Office of Trade Sanctions Implementation (OTSI)

- National Economic Crime Centre (NECC)

- Crown Prosecution Service (CPS)

- Serious Fraud Office (SFO)

- Border Force

- Regional Organised Crime Units (ROCUs)

- Metropolitan Police Service (Counter Terrorism Command)

- Companies House

- Insolvency Service

Equip your team for effective AML/CFT compliance

Strengthen awareness, improve judgement, and build confidence through practical AML/CFT training

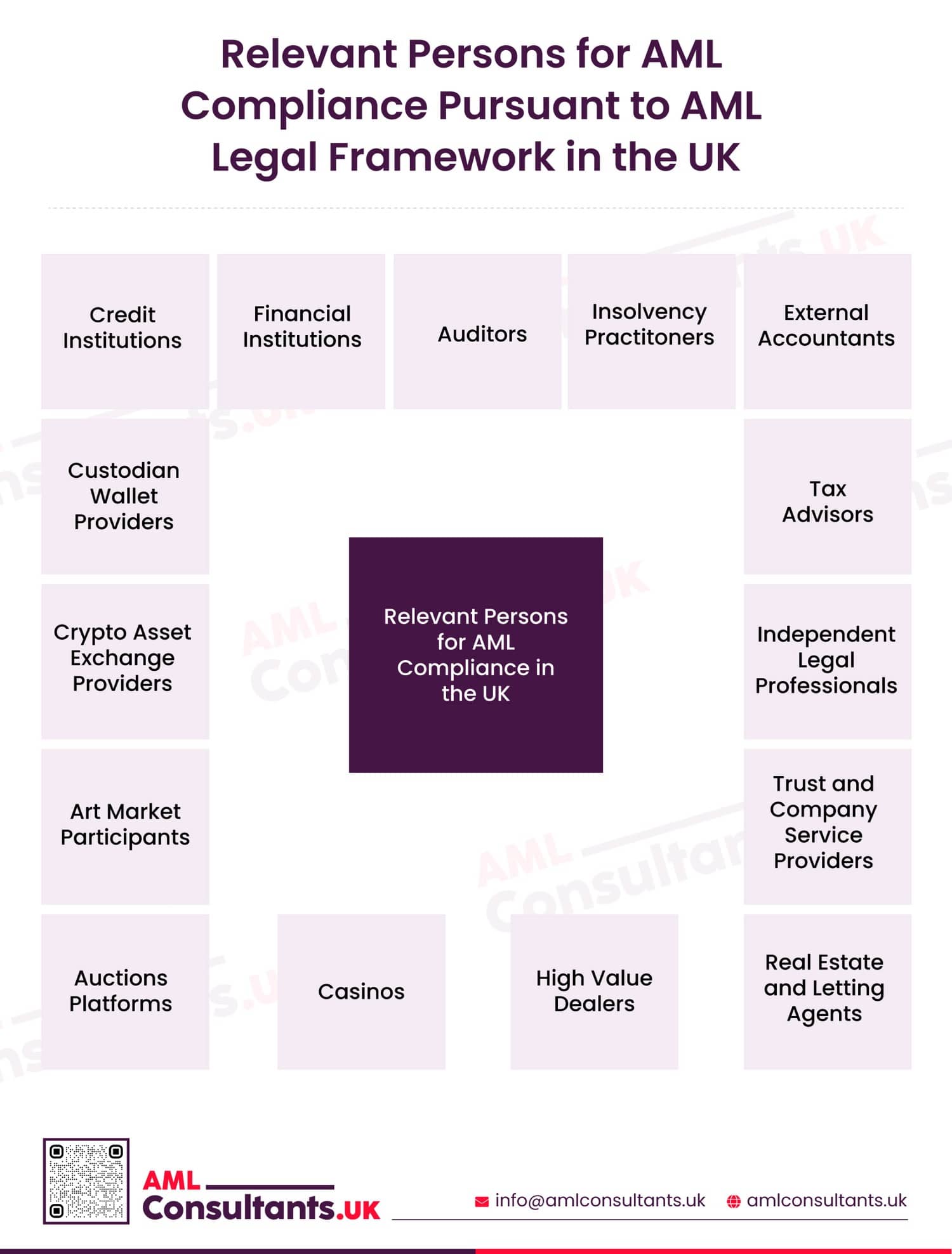

Relevant Persons for AMLCompliance Pursuant to AML Legal Framework in the UK

Businesses categorised as Relevant Persons under Regulation 8 of the MLR, 2017, are obligated to implement an inclusive AML framework and must comply with the directives issued by their relevant supervisory authorities.

The businesses classified as Relevant Persons within AML Legal Framework in the UK are financial institutions, credit institutions, auditors, tax advisors, insolvency practitioners, independent legal professionals, accountants, TCSPs, high value dealers, real estate and letting agents, art market participants, auction platforms, casinos, crypto asset exchange providers and custodian wallet providers.

Credit Institutions

As per Regulation 10 (1) of MLR 2017, Credit Institution means an entity as defined under the Capital Requirements Regulation that accepts deposits or other repayable funds from the public or grants credit or loans for its own account.

Financial Institutions

As per Regulation 10(2) of MLR 2017, “financial institution” refers to a business that carries out one or more financial activities listed in Schedule 2 of the Regulation, including Money Service Businesses. However, it excludes credit institutions and certain exempt entities specified in the Regulations.

The term also covers authorised persons under FSMA, 2000, providing insurance or investment services, collective investment schemes, insurance intermediaries, UK branches of such entities, and certain government savings bodies.

Auditors

As per Regulation 11 (a) of MLR 2017, an auditor is a firm or individual who is a statutory auditor under the Companies Act 2006, carrying out statutory audit work, or a local auditor under the Local Audit and Accountability Act 2014, carrying out an audit required by that Act.

Insolvency Practitioners

As per Regulation 11 (b) of MLR 2017, an Insolvency Practitioner means a firm or individual who acts as an insolvency practitioner under the Insolvency Act 1986 or under the Insolvency (Northern Ireland) Order 1989.

External Accountants

As per Regulation 11 (c) of MLR 2017, External Accountant means a firm or sole practitioner who, by way of business, provides accountancy services to other persons.

Tax Advisers

As per Regulation 11 (d) of MLR 2017, Tax Adviser means a firm or sole practitioner who, by way of business, provides advice on the tax affairs of other persons.

Independent Legal Professionals

As per Regulation 12 (1) of MLR 2017, an Independent Legal Professional is a firm or sole practitioner providing legal or notarial services by way of business, when participating in financial or real estate property transactions, including company or trust formation, management of client assets, or related arrangements.

Trust or Company Service Providers

As per Regulation 12 (2) of MLR 2017, a Trust or Company Service Provider is a firm or sole practitioner who, by way of business, forms companies or other legal persons, provides registered office or similar services, or acts (or arranges another to act) as a director, partner, trustee, or nominee shareholder.

Estate and Letting Agents

As per Regulation 13(1) of MLR 2017, an estate agent is a firm or sole practitioner carrying out “estate agency work” under the Estate Agents Act 1979, including transactions involving interests in land in the UK or overseas where capable of separate ownership.

Regulation 13 (3) of MLR 2017 defines a Letting Agent as a firm or sole practitioner that carries out letting agency work, acting on instructions from prospective landlords or tenants to arrange the letting of land for a term of 1 month or more, where the rent is 10,000 Euros or more per month.

High Value Dealers

As per Regulation 14 (1)(a) of MLR 2017, a high-value dealer is a firm or sole trader trading in goods who makes or receives cash payments of 10,000 euros or more (in a single or linked transactions) in the course of business.

Casinos

As per Regulation 14 (1) (b) of MLR 2017, a casino is a holder of a casino operating licence under the Gambling Act 2005.

Auction Platforms

As per Regulation 14 (1) (c) of MLR 2017, an auction platform is a platform that auctions two-day spot or five-day futures emission allowances, within the meaning of the UK Auctioning Regulation, when carrying out activities covered by that regulation.

Art Market Participants

As per Regulation 14 (1) (d) of MLR 2017, Art Market Participant is a firm or sole practitioner who, by way of business, trades in, intermediates or stores work of art where the value of the transaction, linked transaction or stored artwork is 10,000 Euros or more.

Crypto Asset Exchange Providers

As per Regulation 14A (1) of MLR 2017, Crypto Asset Exchange Provider means a firm or sole practitioner who, by way of business, provides services to exchange crypto assets for money or money for crypto assets, exchange one crypto asset for another or operate automated machines that enable crypto to money or money to crypto exchanges.

Custodian Wallet Providers

As per Regulation 14A (2) of MLR, 2017, Custodian Wallet Providers means a firm or sole practitioner who, by way of business, provides services to safeguard and/or administer crypto assets or hold customers’ private cryptographic keys so they can store, manage or transfer their crypto assets.

Regulation 10 to 14A provides for the broader definition of these Relevant Persons and Regulation 15 provides for which activities are not covered for AML/CFT framework.

Implications of National Risk Assessment on AML Legal Framework in the UK

The National Risk Assessment of Money Laundering and Terrorist Financing, July 2025, published by HM Treasury, plays an important role in determining appropriate risk-based measures to combat the risks of financial crimes.

The government conducts a comprehensive survey of businesses across the UK and identifies high-risk businesses prone to ML/TF/PF activities.

Relevant Persons in the UK are mandatorily required to integrate the findings of NRA into their internal AML program and update their risk assessments, policies, procedures and internal controls that reflect the same.

Overall, the UK’s NRA ensures that the AML compliance measures in the UK remain aligned with the global benchmarks set by the Financial Action Task Force (FATF).

AML Guidance Applicable to all Relevant Persons under UK’s AML Laws and Regulations

- UK Financial Sanctions General Guidance January 2026

- HMT Risk assessment of proliferation financing September 2021

- HMT AML and CFT: Supervision Report: 2022-23 (May 2024)

- HM Government Economic Crime Plan 2 2023-26

- Economic Crime Survey 2024

- FDCO OFSI OTSI DoT HMT DBT Starter Guide to UK Sanctions January 2026

- OFSI HMT Guidance Reporting Information to OFSI July 2025

- HMT Guidance Using digital identities with the Money Laundering Regulations February 2026

- MHCLG, HE, MHCLG (2018 to 2021), DLUHC Guide on ‘Know your customer’ guidance – October 2016

How to Navigate This Guide

- Explore the Sector-Specific legal and compliance framework for Relevant Persons:

| Relevant Persons | Supervisory Authority | Legal Framework | Compliance Requirements |

| Credit Institution | FCA | AML/CFT/CPF Legal Framework in the UK for Credit Institutions | AML/CFT/CPF Compliance Requirements for Credit Institutions in the UK |

| Financial Institution | AML/CFT/CPF Legal Framework in the UK for Financial Institutions | AML/CFT/CPF Compliance Requirements for Financial Institutions in the UK | |

| Auction Platforms | AML/CFT/CPF Legal Framework in the UK for Auction Platforms | AML/CFT/CPF Compliance Requirements for Auction Platforms in the UK | |

| Crypto Asset Providers | AML/CFT/CPF Legal Framework in the UK for Crypto Asset Providers | AML/CFT/CPF Compliance Requirements for Crypto Asset Providers in the UK | |

| Custodian Wallet Providers | AML/CFT/CPF Legal Framework in the UK for Custodian Wallet Providers | AML/CFT/CPF Compliance Requirements for Custodian Wallet Providers in the UK | |

| High Value Dealers | HMRC | AML/CFT/CPF Legal Framework in the UK for High Value Dealers | AML/CFT/CPF Compliance Requirements for High Value Dealers in the UK |

| Art Market Participants | AML/CFT/CPF Legal Framework in the UK for Art Market Participants | AML/CFT/CPF Compliance Requirements for Art Market Participants in the UK | |

| Real Estate and Letting Agents | AML/CFT/CPF Legal Framework in the UK for Real Estate and Letting Agents | AML/CFT/CPF Compliance Requirements for Real Estate and Letting Agents in the UK | |

| Trust and Company Service Providers | FCA or HMRC | AML/CFT/CPF Legal Framework in the UK for Trust and Company Service Providers | AML/CFT/CPF Compliance Requirements for Trust and Company Service Providers in the UK |

| Auditors | HMRC or one of the professional bodies listed in Schedule 1 of MLR, 2017. | AML/CFT/CPF Legal Framework in the UK for Auditors | AML/CFT/CPF Compliance Requirements for Auditors in the UK |

| External Accountants | AML/CFT/CPF Legal Framework in the UK for External Accountants | AML/CFT/CPF Compliance Requirements for External Accountants in the UK | |

| Tax Advisors | AML/CFT/CPF Legal Framework in the UK for Tax Advisors | AML/CFT/CPF Compliance Requirements for Tax Advisors in the UK | |

| Insolvency Practitioners | Insolvency Practitioners Association | AML/CFT/CPF Legal Framework in the UK for Insolvency Practitioners | AML/CFT/CPF Compliance Requirements for Insolvency Practitioners in the UK |

| Independent Legal Professionals | One of the professional bodies listed in the Schedule 1 of the MLR, 2017 | AML/CFT/CPF Legal Framework in the UK for Independent Legal Professionals | AML/CFT/CPF Compliance Requirements for Independent Legal Professionals in the UK |

| Casinos | Gambling Commission | AML/CFT/CPF Legal Framework in the UK for Casinos | AML/CFT/CPF Compliance Requirements for Casinos in the UK |

Spot AML/CFT gaps before regulators do

Review your AML/CFT framework, controls, and documentation to identify areas that need strengthening

How AML Consultants UK Assist in Implementing UK’s Complex AML Legal Framework Smoothly

AML Legal Framework in the UK requires more than just an understanding of legislation; it necessitates that Relevant Persons translate these legal requirements into robust internal controls. AML Consultants UK supports businesses in the UK to navigate complex obligations by offering a wide range of specialised services tailored to relevant sectors.

AML Consultants UK helps Relevant Persons to identify and assess the ML/TF/PF risks exposure their business faces through its Firm-Wide Risk Assessment services. With AML, CTF, CPF Policies, Controls and Procedures Documentation services, it assists Relevant Persons to establish the internal framework for compliance in line with UK’s AML Laws and Regulations.

It also offers several other services, such as Customer Due Diligence Services and KYC Remediation Services that support Relevant Persons to strengthen their customer onboarding, customer risk assessment and ongoing monitoring processes.

In addition, Sanctions Compliance Consultancy services facilitate Relevant Persons to fulfill their sanctions obligations under SAMLA 2018 robustly. It’s AML Software Selection Services supports Relevant Persons to implement AML tools and calibrate their rules.

AML Consultants UK also offers AML, CTF, CPF Training, on UK’s AML Laws and Regulations through which Relevant Persons can equip their staff with the knowledge of UK’s comprehensive AML legal framework.

Integrate Digital Identity in the Right Way!

Build a Robust AML Compliance Program with AML Consultants UK’s Expert Services

FAQs: Frequently Asked Questions

What is the AML Legal Framework in the UK?

AML Legal Framework in the UK comprises various laws and regulations. Sanctions and Anti-Money Laundering Act (SAMLA, 2018), The Money Laundering, Terrorism Financing, Transfer of Funds (Information on the Payer) Regulations 2017 (MLR 2017), Proceeds of Crime, 2002 and several other acts together combine to build a comprehensive legal framework for AML in the UK.

Which authorities enforce UK’s AML Laws and Regulations?

UK’s AML Laws and Regulations are enforced by several supervisory authorities and law enforcement agencies. Supervisory Authorities such as FCA, HMRC, and the Gambling Commission oversee AML/CFT/CPF compliance in various regulated sectors. Law Enforcement Agencies, such as NCA and FIU, ensure that investigations and financial intelligence are handled, while sanctions implementation is overseen by OFSI.

What obligations do businesses have under the UK’s AML Laws and Regulations?

Businesses are obligated to perform the following compliance requirements under UK’s AML Laws and Regulations:

- Registration with their relevant Supervisory Authority

- Appointment of Nominated Officer

- ML/TF/PF Risk Assessment

- Establishment of Internal Policies, Procedures and Controls

- Customer Due Diligence and Customer Risk Assessment

- Sanctions Compliance

- Suspicious Activity Disclosures

- Independent Audit Function

- Record-Keeping

- Training